How To Price Products For Optimal Profit: Our Ultimate Guide & Expert Tips

By Sam Nguyen

Drive 20-40% of your revenue with Avada

In this ultimate guide, we show you how to price products, what factors to consider, and common mistakes to avoid, ensuring you maximize your profitability.

Key Takeaways

- Always ensure that your prices cover your costs. This is fundamental to successful product pricing, particularly for retail items.

- Recognize that your pricing is influenced by your industry’s market dynamics and the competition in your space. Keeping your prices competitive and up-to-date is essential.

- Understand that pricing is not a one-size-fits-all concept. What works for your business may not work for someone else’s, so tailor your pricing strategy to align with your unique circumstances.

Before You Start

New sellers or small businesses often struggle with pricing products, especially now that markets are more competitive than ever. Nine out of 10 consumers price check products on ecommerce platforms, so it’s easy to understand why there’s so much pressure on getting your pricing right. Before pricing your products, you need to understand your business and the market.

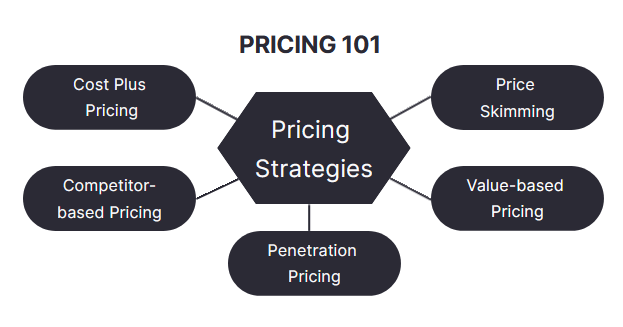

Understanding Pricing Strategies

Pricing strategies are essential for businesses to determine the optimal price for their products or services. Each strategy has distinct advantages and considerations. Here’s a breakdown of various pricing strategies:

- Cost-based Pricing: This strategy starts with understanding the total cost of production. It ensures you cover your expenses while making a profit.

- Competitor-Based Pricing: Spy on your competitors and adapt your pricing to stay competitive. For example, a new coffee shop enters a neighborhood dominated by established cafes. To attract customers, they price their coffee slightly lower than the competition.

- Value-Based Pricing: Focuses on the perceived value of your product in the eyes of the customer, allowing you to charge more for products with higher perceived value.

- Demand-Based Pricing: Adjust prices based on demand fluctuations. Raise prices during peak seasons and lower them during off-peak times.

- Manufacturer Suggested Retail Pricing: Follow the pricing recommendations a product manufacturer provides to maintain consistency across retailers.

- Premium Pricing: Charge higher prices to create an aura of luxury and exclusivity around your brand or product.

- Psychological Pricing: Use psychological tactics to influence consumer perception, including

- Charm Pricing: Selling a product for $9.99 instead of $10 to make it seem like a better deal.

- The 100 Rule: Using percentage discounts for items under $100 and dollar discounts for items over $100.

- Discounts & Special Offers: Offering “buy one, get one free” deals during holiday seasons.

- Price Anchoring: Presenting a high-priced product initially to make subsequent, lower-priced options seem more attractive.

- Bundle Pricing: Combine multiple products or services into a single package at a discounted rate compared to buying items individually.

- Penetration Pricing & Skimming:

- Penetration Pricing: Set low initial prices to quickly gain market share and outcompete rivals.

- Skimming: Start with high initial prices to target early adopters and recoup development costs before gradually lowering prices. Choosing the right pricing strategy is like finding the perfect note in a symphony—it requires harmony and precision. By understanding these strategies and aligning them with your business goals, you can strike the right chord with your customers and maximize profits.

Conducting Market Research

Here’s a creative and easy-to-understand guide to conducting market research:

Before diving into product pricing, starting with robust market research is imperative. Understanding the market landscape gives you a clearer picture of where your product stands in relation to competitors. Start by identifying similar products or services in the market. Note their price points and the value they offer. This comparative analysis can offer insights into prevailing market rates and potential gaps your product might fill.

You can also examine your competitors’ pricing. Identify both the highest and lowest prices you encounter. Unless your product has a unique edge that justifies a higher cost, it’s probably best not to exceed the highest price you find.

Additionally, consider getting feedback from friends, family, and colleagues. Ask them about their price expectations for your product or similar items. Which competitor’s price seems most appealing to them? Their responses can offer a practical perspective on the expected price range for your product.

Furthermore, it’s beneficial to gauge customer perspectives. Surveys, feedback forms, or even casual conversations can reveal how much customers are willing to pay for a product like yours. By understanding their budget constraints and the value they place on your product’s unique features, you’re better positioned to set a competitive price.

Economic indicators and trends can also play a role. If the economy is booming, consumers might be more willing to splurge, but during a downturn, cost-cutting becomes essential. So, keeping an eye on larger economic shifts and tailoring your pricing strategy accordingly can be a wise approach.

Lastly, always be prepared to adjust. The initial price point might require tweaking based on real-time sales data, feedback, and changing market dynamics. Thus, considering market research as an ongoing process rather than a one-time task will ensure your pricing remains relevant and competitive.

How To Price A Product

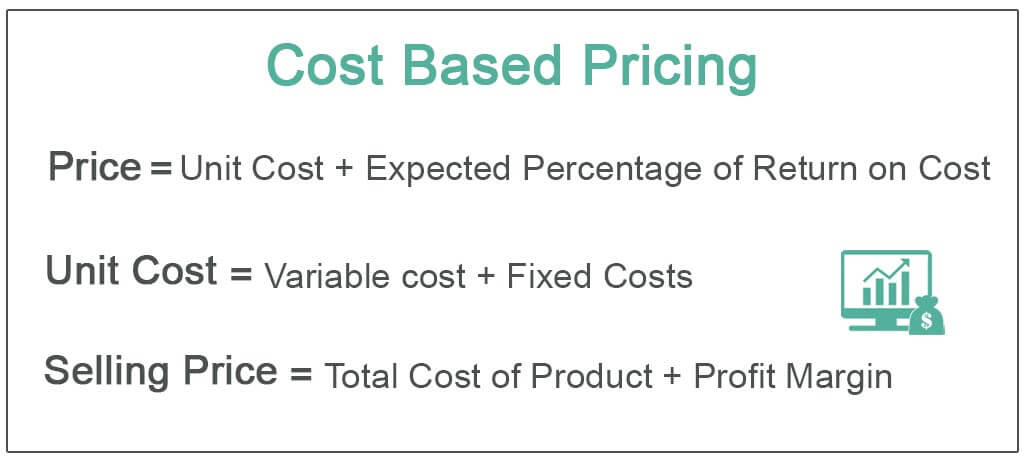

Cost-based Pricing

Add up your variable costs (per product)

Understanding your costs is a fundamental pillar of an effective pricing strategy. Whether you purchase or craft products yourself, accurately calculating your variable costs per product is key. Let’s walk through this process step by step:

Know Your Cost of Goods Sold (COGS): If you purchase products, determine the cost of each unit, which constitutes your COGS. This is the starting point for your variable costs.

For Product Makers - Unveil Comprehensive Costs: For those creating products, delve deeper into the production components:

- Raw Materials: Sum up the cost of all materials needed for a bundle of products.

- Labor Costs: Factor in the labor needed to create the bundle of products.

- Overhead Costs: Include any other overhead costs associated with production.

Calculate costs of your selling platform: Remember to include the fees associated with your sales channels. For instance, if you’re selling online via Shopify, make sure to calculate platform’s charges. Similarly, for offline sales, incorporate your lease expenses.

Value Your Time: Acknowledge the value of your time spent on the business. Set an hourly rate that you aim to earn from your venture. Divide this rate by the number of products you can craft in an hour. Incorporate this as a variable cost to ensure a sustainable price.

Consider Additional Variable Costs: Account for other variable costs such as packaging, promotional materials, shipping, and affiliate commissions. Add these to your per-product cost calculation.

Summing Up the Variables: Combine the COGS per item, the value of your time, and the additional variable costs to arrive at the total per-product cost.

For example: COGS per candle: $6.00 Labor cost: $75 Packaging cost: $25 Advertising cost: $20 Total Variable Costs per Candle: $6.00 + $75 + $25 + $20 = $126.00

In this example, the total per-product cost, including all the variable components, amounts to $$126.00. This figure is fundamental for establishing a competitive yet sustainable pricing strategy. Always consistently align your pricing with what your target customers are willing to pay, making informed decisions through meticulous market research.

Add in your profit margin

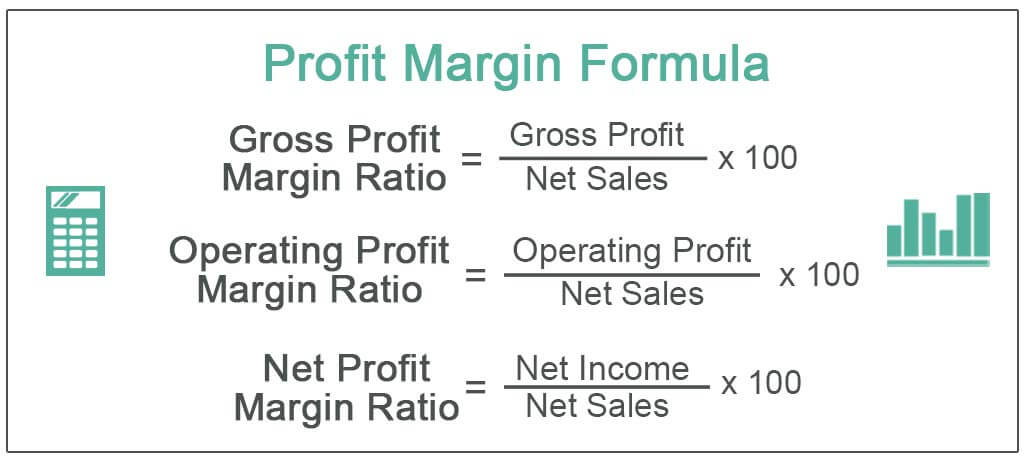

Profit margin is a key financial metric that represents the percentage of profit your business earns from each sale. It’s a vital indicator of your business’s financial health and efficiency. To calculate it, you can follow these steps:

- Input Your Item(s) Cost:** Enter the total cost of each item you intend to sell. This should encompass production costs, materials, and any product creation expenses.

- Decide Your Profit Percentage:** Determine the profit percentage you aim to earn on each sale. This profit should be in addition to covering the production cost of each item.

- Compute Profit:** After inputting the necessary information, utilize a Profit Margin Calculator. This tool uses an algorithm to recommend an optimal selling price for your product, considering your set profit percentage.

- Establish Your Pricing:** The calculator will provide a pricing recommendation based on your input. Charging this price ensures you cover your costs, achieve your desired profit, and remain competitive.

The profit margin formula is fundamental for understanding your business’s profitability. It’s calculated by dividing the gross profit margin by net revenue and then multiplying by 100:

Profit Margin = (Gross Profit / Net Revenue) x 100

The ideal profit margin varies depending on your industry, business model, and market dynamics. Generally, a higher profit margin signifies better financial health and operational efficiency.

Lower profit margins may be the norm in industries with high operating costs or intense competition. Conversely, sectors with unique products or services and limited competition may experience higher profit margins.

To assess whether your profit margin is healthy, it’s crucial to compare it to industry benchmarks and your competitors. Consider factors like your business’s growth goals, market share, and overall financial stability when evaluating your profit margin.

While the terms “margin” and “markup” are sometimes used interchangeably, they have distinct meanings in business finance:

- Margin: Margin represents the profit percentage after subtracting the cost of goods sold from revenue. It focuses on the relationship between profit and revenue.

- Markup: Markup is the amount added to the cost of goods to establish the selling price. It is expressed as a percentage of the cost. Markup centers on the relationship between the cost of goods and the selling price.

In essence, margin measures profitability based on revenue, while markup is a pricing measure based on cost. Understanding these distinctions is crucial for making informed pricing decisions.

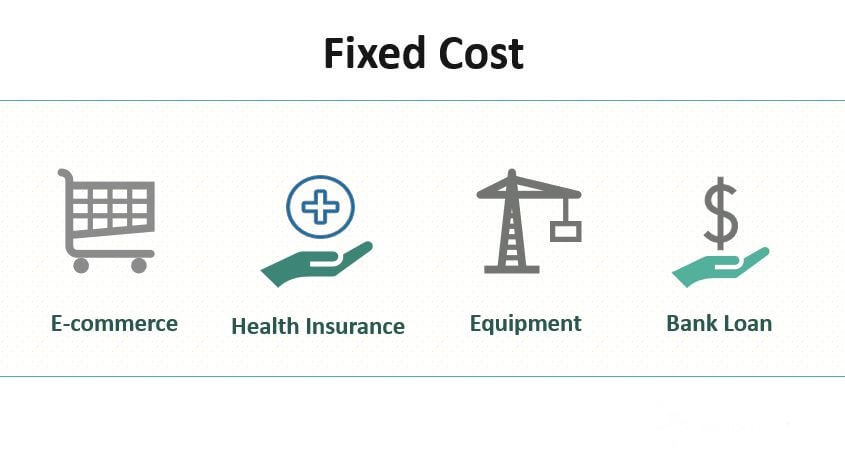

Factor in fixed costs

Fixed costs, also known as overhead costs, are expenses that remain constant regardless of changes in production or sales volume. These costs are incurred regularly to keep your business running but do not vary with the production level. Common examples of fixed costs include rent or lease payments, salaries of permanent staff, insurance premiums, and utilities.

Key Considerations:

- Consistency: Fixed costs remain stable over time, providing a degree of predictability in your financial planning.

- Business Survival: Paying fixed costs is essential to maintain business operations, even during lower sales or production periods.

- Pricing Impact: Failing to account for fixed costs in your pricing strategy can lead to underpricing, which may jeopardize your business’s financial sustainability.

For example, you operate a small bakery, and your fixed costs include monthly rent of $1,500, a salaried baker earning $2,500, and utility bills averaging $200. You produce various types of bread.

Step 1: Identify Fixed Costs:

- Rent: $1,500 per month

- Baker’s Salary: $2,500 per month

- Utilities: $200 per month

Step 2: Calculate Total Monthly Fixed Costs:

Rent + Baker’s Salary + Utilities = $1,500 + $2,500 + $200 = $4,200 Your total fixed costs amount to $4,200 per month. This is the minimum amount your bakery needs to cover to remain operational, regardless of the quantity or type of bread you produce.

Step 3: Distribute Fixed Costs Across Products:

To incorporate fixed costs into your pricing strategy, you’ll need to distribute them across the products you offer. Let’s say you produce three types of bread: White Bread, Whole Wheat Bread, and Rye Bread.

Calculate the proportion of fixed costs allocated to each product by dividing the product’s revenue by the total revenue of all products.

Example Calculation:

- White Bread revenue per month: $3,000

- Whole Wheat Bread revenue per month: $2,000

- Rye Bread revenue per month: $1,500

- Total revenue: $3,000 + $2,000 + $1,500 = $6,500

Allocate fixed costs:

- White Bread’s share of fixed costs: ($3,000 / $6,500) x $4,200 = $1,938.46

- Whole Wheat Bread’s share of fixed costs: ($2,000 / $6,500) x $4,200 = $1,284.62

- Rye Bread’s share of fixed costs: ($1,500 / $6,500) x $4,200 = $976.92

Step 4: Add Fixed Costs to Product Costs:

Finally, add each product’s fixed cost share to its variable production cost. This total cost per product should cover all expenses, including variable and fixed costs while ensuring profitability.

- Example Calculation for White Bread:

- Variable production cost of White Bread: $2.50

- Total cost per loaf of White Bread: $2.50 + $1,938.46 = $1,940.96

By factoring in fixed costs and distributing them across your products, you can set prices that not only cover your production expenses but also contribute to covering your monthly overhead, ensuring the sustainability of your bakery business.

Test and adjust accordingly

Setting the right price for your products isn’t a one-time task; it requires constant monitoring and adjustments. Once you’ve figured out your costs and applied some pricing tactics, remember that prices can always be changed based on various factors. Continuously test different price points and gather customer feedback to ensure optimal pricing.

Consider the following scenarios for potential price adjustments:

-

Launching New Products: When rolling out new items, it’s okay to price them a bit higher than your older products. Conversely, if feasible, consider reducing the prices of your existing products. This strategy can make older items more enticing while highlighting the value of the new arrivals.

-

Increase in Production Costs: Should your production expenses rise, it’s crucial to reassess your pricing. You might have set some margins earlier, but if they’re getting squeezed, it’s essential to ensure your selling price remains profitable. If your products are on the higher end price-wise, exploring ways to reduce costs without compromising quality could be beneficial.

-

Market Changes: External factors, such as market fluctuations or new competitors entering the scene, may necessitate price adjustments. To remain competitive, you need to stay attuned to these shifts. Balancing a price that appeals to customers yet implies value can be challenging. However, by continuously monitoring the market, you’ll be better positioned to find that sweet spot.

Factor in Psychological Pricing

Psychological pricing takes advantage of human psychology to influence purchase decisions. Here’s how it works with some examples:

- Charm Pricing: Set prices slightly below round numbers (e.g., $9.99 instead of $10) to make them seem more appealing.

- The 100 Rule: Use percentages for lower-priced items (e.g., 25% off) and exact amounts for higher-priced items (e.g., $100 off) to highlight perceived savings.

- Discounts & Special Offers: Create a sense of urgency by offering limited-time discounts or bundle deals.

- Price Anchoring: Present a premium option first (e.g., “Gold Package: $499”) to make other choices seem more affordable (e.g., “Silver Package: $299”).

Consider Other Pricing Techniques

- Bundle Pricing: Combine related products or services into packages (e.g., “Buy two, get one free”).

- Penetration Pricing: Start with lower prices to gain market share or introduce new products (common in tech and electronics).

- Skimming: Begin with higher prices for early adopters and gradually reduce them over time (often seen in fashion and luxury industries).

Which Factors To Consider When Pricing Your Products?

Market Demand

Understanding the demand for your product is paramount. Consider:

- Customer Perception: How do your target customers perceive the value of your product?

- Market Trends: Are there seasonal or industry-specific trends that affect demand?

- Elasticity: How sensitive is demand to price changes? Will lower prices significantly increase sales, or will customers still buy at a higher price?

Competitor Pricing

Your competitors’ pricing strategies can provide valuable insights:

- Competitive Landscape: Analyze the pricing strategies of your direct and indirect competitors.

- Unique Selling Proposition (USP): Determine if your product offers unique features or quality that justifies a premium price or if you need to be competitive on price.

- Price Positioning: Decide whether you want to position your product as a low-cost option, a premium choice, or somewhere in between.

###Target Audience

Your pricing strategy should align with the preferences and purchasing power of your target customers:

- Customer Segmentation: Consider different customer segments and their price sensitivity.

- Price Sensitivity Analysis: Determine how much your customers are willing to pay for your product.

- Value Perception: Understand how your target audience perceives the value of your product and how it fits into their needs and lifestyle.

Distribution Channels

The channels through which you sell your products can impact pricing:

- Channel Markups: Evaluate the markups and fees associated with different distribution channels, such as retail stores, online marketplaces, or direct sales.

- Channel Margin Expectations: Determine the margins expected by intermediaries in the distribution chain.

- Pricing Consistency: Ensure your pricing is consistent across all distribution channels to maintain trust and avoid conflict.

Common Mistakes in Pricing A Product

Underpricing or Overpricing:

Consequences:

- Underpricing: You may struggle to cover your costs, eroding your profitability and long-term sustainability. Customers might also perceive low prices as indicative of low quality.

- Overpricing: Your target audience may deem your product unaffordable, leading to missed sales opportunities. It can also create a perception that your product is overvalued, making it difficult to compete.

Neglecting Inflation and Production Cost Changes:

Consequences:

- Reduced Margins: Ignoring cost increases can lead to shrinking profit margins, making it challenging to maintain business profitability.

- Price Shock: Suddenly raising prices to compensate for cost changes can alienate loyal customers and cause resentment.

Ignoring Customer Feedback:

Consequences:

- Lost Opportunities: Ignoring customer input can result in missed opportunities for improving your pricing structure to align with your audience’s values.

- Customer Dissatisfaction: Customers may become frustrated if their feedback is consistently disregarded, leading to a decline in loyalty and negative word-of-mouth.

Avoiding these common pricing mistakes requires a combination of market research, cost analysis, and active engagement with your customer base. Continuously evaluate your pricing strategy to ensure it remains competitive, profitable, and customer-centric.

Bottom Line

Pricing your products can seem daunting, especially when you’re just starting out in business. However, it doesn’t need to be overwhelming. Conduct competitor research, perform thorough calculations, and craft prices that appeal to your customers. With the right approach, you’ll be well on your way to boosting your sales.

As your business expands and your confidence in pricing strategies grows, you’ll likely discover your own tips, tricks, and insider insights to enhance your pricing game. But for now, our guide is here to provide you with a solid foundation.

In conclusion, we’ve walked you through the essential aspects of establishing the right pricing for your products. It’s not a random process, nor is it magic. We hope our guide has demystified the pricing journey and made it more manageable than you initially imagined.

New Posts